“I came in from the wilderness, a creature void of form.

‘Come in,’ she said, ‘I’ll give you shelter from the storm’” – Bob Dylan

How quickly sentiment can change? As recently as December the pundits were touting 4% GDP and forecasting new highs on the S&P 500 to then a quarter later upping their recession forecast from the normal level around 20% to as high as 48%. Of course, John Kenneth Galbraith always said, “The only function of economic forecasting is to make astrology look respectable” so these forecasts should be taken with a grain of salt. More relevant to our situation is how we have positioned for unexpected volatility. Since almost all aberrant behavior causes volatility, the trick is to position with flexibility and a strong foundation (or “Be Like Water” to reference our October 2025 letter). This is where we think our diversified strategy excels. This is why we added exposure to healthcare and global equities following periods of market weakness, when prices had declined relative to prior levels. It is why we also recommended caution in our fourth quarter 2025 commentary when we said “The disconnect between the scale of projected AI compute needs and the current under-representation of the sectors that must power it creates an attractive setup in our mind. For that reason, we remain constructive on natural resources and energy as durable cash-generative complements to portfolios otherwise dominated by software narratives.” Did we know oil and silver would spike above 100? No! However, we did feel the diversification benefit and the non-correlated, asymmetric upside was worth the investment. Of course, the question then becomes: what is the next play? As exciting as those tactical moves have been, and may continue to be, the more enduring story is how we compound returns in the face of volatility. The diverse, risk-aware portfolio provides ballast amidst market crosscurrents and is where more time should be spent, in our opinion. In fact, we believe the stability provided by a diverse portfolio often allows tactical moves into unloved areas with better risk-return profiles not the other way around.

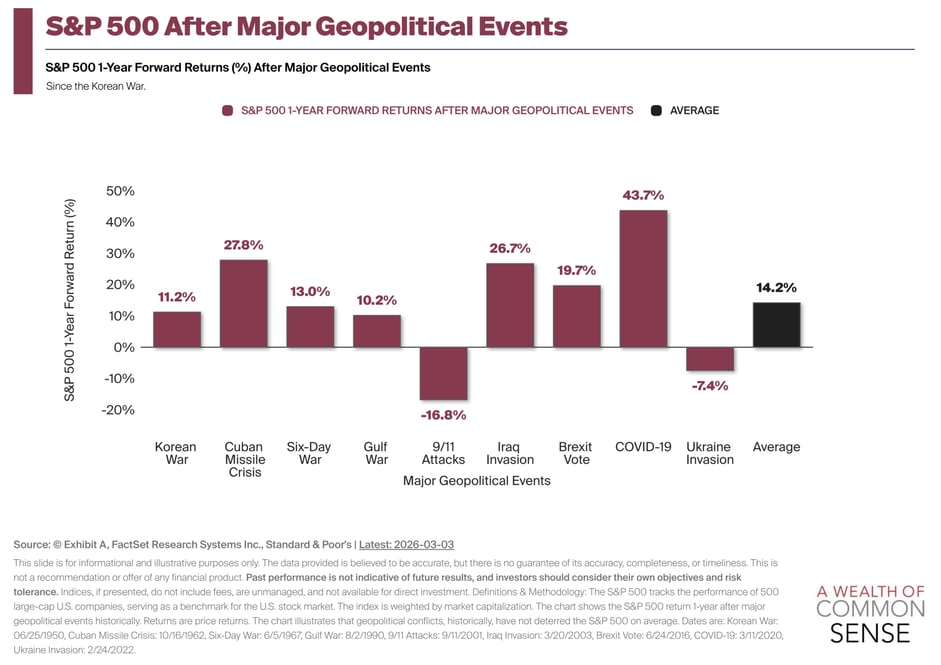

To provide additional context around how markets have historically behaved following periods of heightened uncertainty, we have included a chart that displays performance after some of the riskier moments in history, which inadvertently introduces one of the more important variables in risk and return relationship that many leave out: “time”. The chart displays rates of return a year after major geopolitical events that have occurred over the past 76 years. If you review these, you'll notice the S&P 500 is on average higher 12 months later. Some will say, “this time is different” and we acknowledge that market conditions can differ materially from one period to another. However, we would add that if you look at the worst performing time frame displayed in the chart, beginning September 9th, 2001, and then compare some of our largest “flexible” holdings it may be an even more instructive lesson. Naturally, we must include an obligatory compliance note here that past performance is not indicative of future results, and by choosing three of our biggest “Flexible Mandate/Hedged” holdings rather than a random sample, one could argue that we were “cherry-picking”. As a side note we have selected these holdings because they represent the biggest percentage of our “flexible/hedged” holdings for our clients. We view these positions as components of a diversified portfolio approach that may help support long‑term participation in the market across different conditions. If our goal was simply to show market performance, we would reference long‑only strategies; however, the purpose of this example is to illustrate how different portfolio components may respond in varying market environments. Disclaimers aside, from 09/11/2001 to 9/11/2002, FPA Crescent, First Eagle Global, and T. Rowe Price Capital Appreciation were up, respectively, 10.59%, 12.08%, and 2.15%, while the S&P 500 was down 16.8%. If you carry this further and review the three-year time frame the logic still holds up as FPA Crescent, First Eagle Global, and T Rowe Price Capital Appreciation were up, respectively, 48.28%, 71.46%, and 36.32% versus an S&P 500 that was up 8.18%. Of course, if you take the returns even further out, then you'll see that the S&P return was better (and we are happy to do that if a client requests it), but that's not the point of our exercise. These comparisons are not intended to suggest that any particular outcome will recur. The point is that no matter what strange behavior is going on in the world, we believe that maintaining a diversified, risk‑aware approach can help investors remain engaged with their long‑term plans through a range of market conditions, recognizing that no strategy eliminates risk and that results will vary.

Some people call these diversified portfolios “boring” or “diworsification” and while we respect other’s opinion, we think they are missing nuances to this. Many are confusing a foundational strategy with distractions and salesmanship. Many think boring is complacent and we are certainly not that. Complacent is what makes one pile into private equity with promises of double digit returns and a “Net-Asset Value” that never fluctuates while being wrapped in an expensive, illiquid offering. We wrote about this in 2018 and in 2024 and still believe our stance is appropriate regarding this investment vehicle. We certainly understand the appeal of attractive long-term institutional returns with low volatility but the push to offer these assets to individuals is misguided, at best, in our opinion. Individuals have lumpy, real world cash needs and can’t raise tuition or expenses to then pay their bills, so illiquidity is a bug not a feature, for them. Fortunately, having a convicted strategy allows us the capability to put new and fancy “offerings” through the “sniff” test and pass while the masses herd into the perceived safety of “everyone’s doing it”. Some call this philosophy “Boring you to Wealth” and while we are not completely comfortable with the connotation associated with “boring” we applaud the implication around growing wealth via a sound strategy.

On that note, to quote Bob Dylan, we plan to continue providing a “Shelter from the Storm” approach for years to come as boring as that may sound. Please call to regale us with spring vacations, summer cruises, exhilarating adventures and family milestones so we can share exciting things that matter, not the ups and downs of the market. In the meantime, our efforts remain centered on thoughtful portfolio construction, risk awareness, and ongoing evaluation of market conditions, so you can rest easier amidst the volatility that inevitably presents itself.

General Compliance Disclosures

Statements made via this letter are the opinions of Creative Financial Group (“CFG”) and its advisors, and are not to be construed as guarantees, warranties or predictions of future events, portfolio allocations, portfolio results, investment returns, or other outcomes. None of the information contained is intended as a solicitation or offer to purchase or sell a specific security, mutual fund, bond, or any other investment. Readers should not assume that the considerations, suggestions, or recommendations will be profitable, suitable to their circumstances or that future investment and/or portfolio performance will be profitable or favorable. Past performance of indices, mutual funds, or actual portfolios does not guarantee future results. Future results may differ significantly from the past due to materially different economic and market conditions. SSI, its affiliates and its officers, directors and employees may from time to time acquire, hold or sell securities mentioned herein.

Investment products and services are provided and offered through Synovus Securities, Inc. (SSI), a registered Broker-Dealer, member FINRA/SIPC and an SEC Registered Investment Advisor, Synovus Trust Company, N.A. (STC) and Creative Financial Group, a division of SSI. Trust services are provided by STC, a subsidiary of Pinnacle Bank, a Tennessee bank. Investment products and services are not FDIC insured, are not deposits of or other obligations of Pinnacle Bank, are not guaranteed by Pinnacle Bank, and involve investment risk, including possible loss of principal amount invested. SSI is a subsidiary of Pinnacle Financial Partners, Inc. and an affiliate of Pinnacle Bank, a Tennessee bank, dba Synovus Bank, and an affiliate of STC. You can obtain more information about SSI and its Registered Representatives by accessing BrokerCheck.